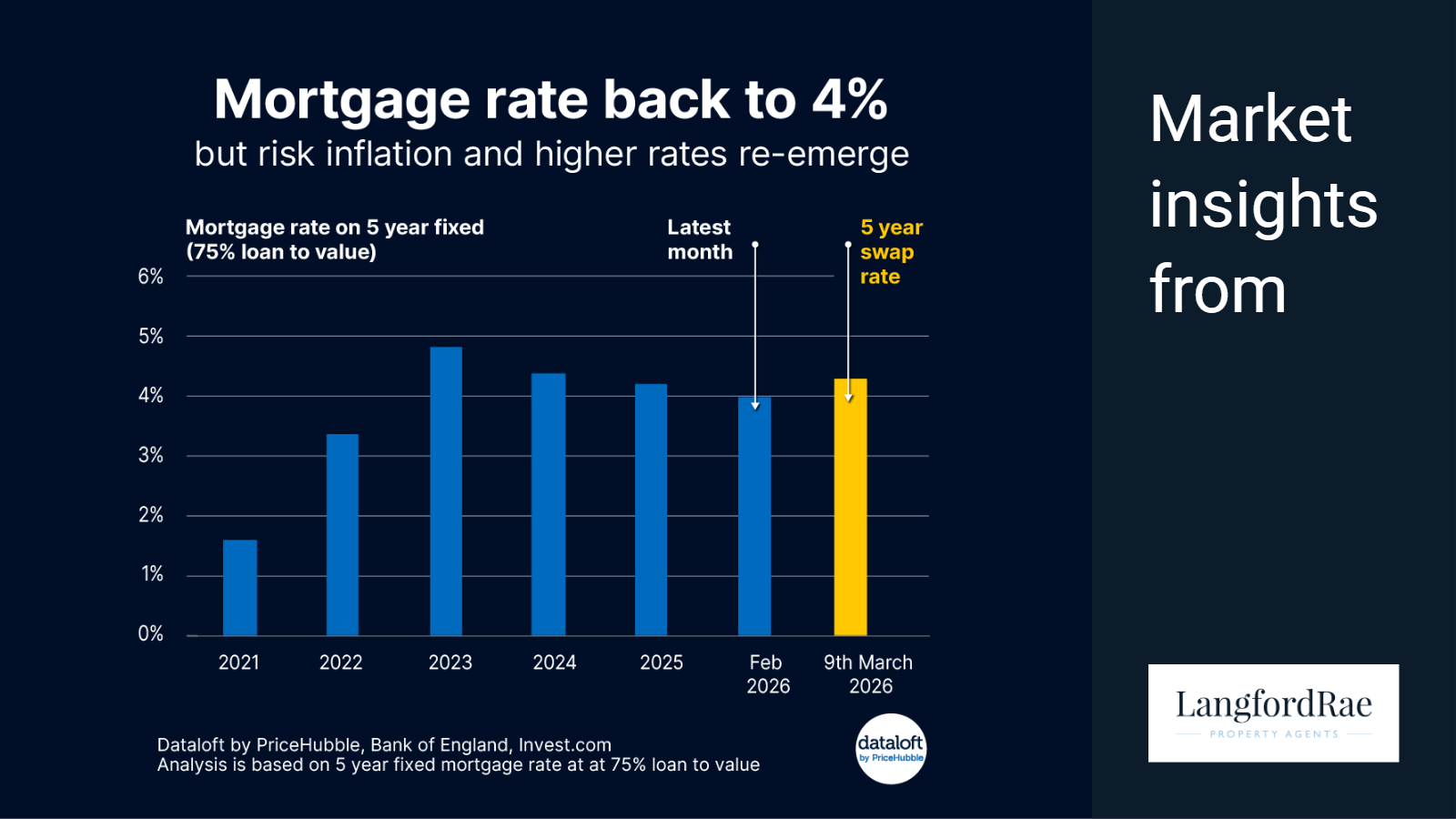

For the first time since mid-2022, the average rate on a five-year fixed mortgage has returned to around 4%. After several years of elevated borrowing costs, the move represents a welcome milestone for prospective buyers and homeowners preparing to remortgage. Yet the improvement may prove fragile, as global economic risks threaten to push borrowing costs higher again.

In early 2026, some of the most competitive two- and five-year fixed mortgage deals briefly dipped below 3.7%, raising hopes that mortgage pricing might soon fall firmly back under the 4% threshold. However, that optimism has already been tested. Rising geopolitical tensions in the Middle East have driven up oil and gas prices, pushing financial market expectations for inflation higher.

The result has been a surge in swap rates, the financial benchmarks lenders use to price fixed-rate mortgages. As swap rates rise, mortgage pricing usually follows. Since early March, several lenders have already begun adjusting their rates upward, making sub-4% mortgage deals less widely available than many expected at the start of the year.

Since this article was written, further developments have highlighted just how quickly mortgage markets can move. The BBC has reported that mortgage rates are already rising again, with lenders pulling products from the market amid turmoil linked to the escalating conflict involving Iran. Meanwhile, The Guardian reports that the average UK mortgage rate has climbed above 5%, as banks rush to reprice loans in response to rising energy prices and higher funding costs triggered by the Middle East crisis. The upheaval has led to hundreds of mortgage deals being withdrawn or repriced in a matter of days, underlining how global events can rapidly feed into the cost of borrowing for UK homeowners.

A “Choppy” Mortgage Market

The outlook for mortgage rates during 2026 is increasingly uncertain. Analysts widely expect conditions to remain volatile or “choppy” until global geopolitical risks settle.

Part of the complexity lies in the broader interest rate environment. The Bank of England held the base rate at 3.75% in February 2026, after a series of earlier increases aimed at controlling inflation. Financial markets still anticipate that rate cuts could arrive later in 2026 if inflation continues to ease and economic growth slows.

If the Bank does begin cutting rates, mortgage costs should gradually follow. Some forecasts suggest average mortgage rates could drift below 3.5% during 2026 if monetary policy loosens and financial markets stabilise.

However, the path is unlikely to be smooth. International investment banks remain cautious. Strategists at Morgan Stanley, for example, believe that global bond yields could fall during 2026 before rising again later in the year and into 2027. That scenario could push longer-term mortgage rates back upward after an initial period of decline.

Are Mortgage Rates Likely to Fall Below 4%?

Short-term expectations suggest it is possible. If the Bank of England cuts the base rate and inflation continues to moderate, mortgage deals below 4% may become more common again. Earlier in 2026 the market briefly saw rates as low as 3.7%, showing how quickly pricing can shift when market sentiment improves.

However, the current rise in swap rates highlights how vulnerable mortgage pricing is to global events. In other words, lower rates remain possible but they are far from guaranteed.

Will Mortgage Rates Reach 5% in 2027?

Global forecasts point to a mixed outlook. Morgan Stanley expects benchmark government bond yields to fall initially before rising again during the second half of 2026 and into 2027. If that occurs, longer-term mortgage rates could move back towards the 5.5% range globally, demonstrating that the era of ultra-cheap borrowing is unlikely to return soon.

Fixed Rates vs Tracker Deals

Borrowers considering a new mortgage are also weighing up whether to fix their rate for a shorter or longer period.

A five-year fixed mortgage remains a popular option for homeowners seeking certainty and predictable repayments. Locking in for longer can provide protection against unexpected rate increases if inflation or geopolitical risks push borrowing costs higher again.

By contrast, tracker mortgages move in line with the Bank of England base rate. From January 2026, some lenders have already reduced their standard variable rates and tracker products as the base rate stabilised.

How Borrowers Can Access Lower Mortgage Rates

Securing the most competitive mortgage rate typically depends on several financial factors. Borrowers who wish to access rates around or below 4% often need:

-

A larger deposit or substantial home equity

-

A strong credit history

-

A lower debt-to-income ratio

-

The option to buy discount points or rate reductions

-

Access to specialist mortgage products arranged through brokers

Lenders will usually reserve the lowest rates for borrowers with at least 25% equity or deposit, meaning the most competitive deals may not be available to everyone.

Timing Matters

One advantage for borrowers is that many lenders allow new mortgage rates to be secured up to six months in advance. In a volatile market, locking in a deal early can provide protection against potential rate rises while still allowing time to complete a purchase or remortgage.

Seek Professional Advice

Given the speed at which mortgage markets can change, particularly during periods of global economic uncertainty, borrowers should always seek independent advice from a qualified mortgage broker or regulated lender before applying for a mortgage or switching products.

While the return of a 4% mortgage rate marks a notable moment in the market, the wider economic environment suggests borrowing costs may continue to move unpredictably in the months ahead.

Sources: Dataloft by PriceHubble, Bank of England, Invest.com. Analysis based on five-year fixed mortgage rates at 75% loan-to-value.

Share this article

More Articles

Sign up for our newsletter

Subscribe to receive the latest property market information to your inbox, full of market knowledge and tips for your home.

You may unsubscribe at any time. See our Privacy Policy.